NEW YORK, July 30, 2019 - This page summarizes a TIAA-sponsored MIT AgeLab study published in 2019. At that time, a large majority of American adults (84%) reported that student loans were reducing how much they could save for retirement. Nearly three out of four (73%) borrowers said they were delaying stronger retirement savings until loans were paid off. Among people who were not saving for retirement at all, more than one quarter (26%) cited paying student loan debt as the reason.

The yearlong project looked at student loan debt, longevity planning, and family dynamics. It showed that life stage and who the loans were taken out for shaped how households balanced loan repayment with retirement saving.

Borrowers of all ages, including parents and grandparents, reported financial tradeoffs tied to repayment. Among 25- to 35-year-olds who were not saving for retirement, 39% said they were prioritizing student loan payments. Among parents and grandparents borrowing for children or grandchildren, 43% said they would increase retirement savings after the student loan was repaid. In focus groups, women in particular described putting children’s education and wellbeing ahead of their own retirement security.

“To be sure, getting a college degree remains one of the smartest investments a person can make in their financial future - but saving for retirement is equally important,” said Roger W. Ferguson, Jr., then president and CEO of TIAA. “We believe that advice and coaching are key to navigating what can seem like competing demands. TIAA has found that people who engage with qualified financial professionals are better equipped to make decisions about paying for education for themselves or a loved one without sacrificing their future financial security.”

These 2019 findings remain a useful snapshot for reporters, educators, and families reviewing how loan obligations interact with long-term saving. Use the downloads on this microsite for the executive summary, three issue briefs, and the print-friendly press release.

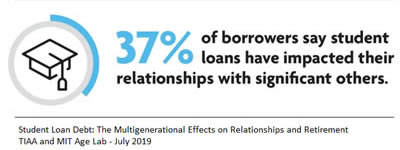

|